2025 Third Quarter Market Commentary

The third quarter saw strong market gains with both the U.S. and international stock markets hitting new highs. In the U.S., performance was driven by several key factors: robust corporate earnings growth, the Federal Reserve’s first interest rate cut of the year, and continued momentum in artificial intelligence (AI) innovation. A decline in U.S. interest rates also lifted fixed income returns, with U.S. bonds showing particularly strong performance year-to-date.

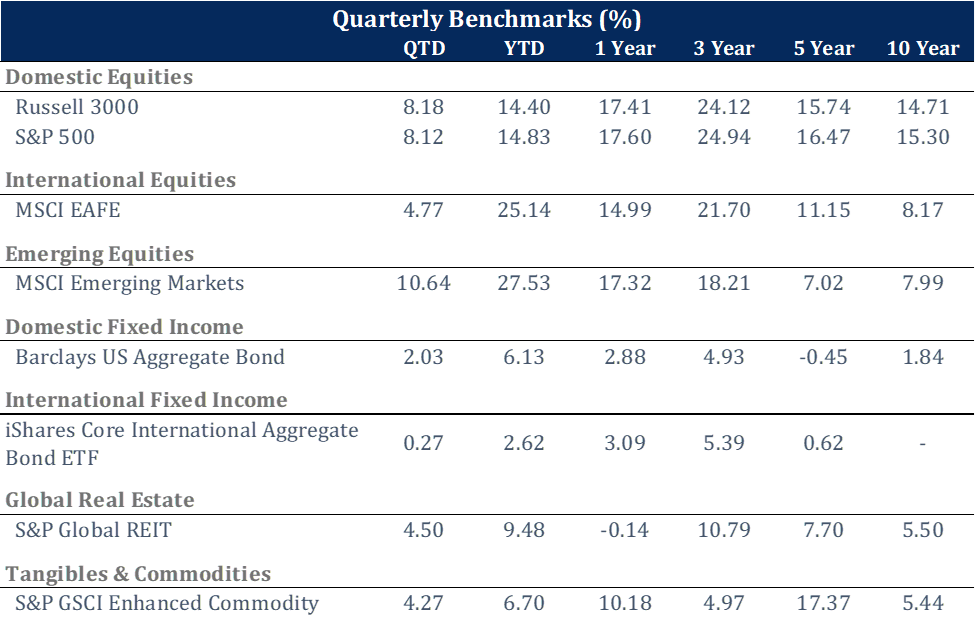

Below is a breakdown of returns of the major investment categories across our client portfolios:

Historically, stock market returns tend to follow the trajectory of corporate profits, and 2025 has been no exception. Over 80% of S&P 500 Index companies exceeded analyst expectations for profits in the second quarter, marking the third consecutive quarter of double-digit earnings growth. While daily headlines often focus on potential risks, long-term market performance is ultimately driven by these profits. And when these profits surpass expectations, it is typically good news for investors.

More good news has come from the world of AI, where investor enthusiasm has surged as more people integrate language models and other AI tools into their daily lives. While large U.S. technology firms have been the most visible beneficiaries, the impact of AI investment spans a wide range of industries from data centers and chipmakers to utility providers. These gains are not limited to the stock market; AI investment is also fueling economic growth. In the first half of 2025, AI contributed $152 billion to U.S. GDP growth. This is nearly double the $77 billion contribution from consumer spending, which has traditionally been the primary driver of economic expansion.

With AI boosting worker productivity, many economic pundits are keeping a close eye on the labor market. The unemployment rate remains low at 4.3%, but job creation has slowed. Only 22,000 new jobs were added in August, a sharp decline from the monthly average of 123,000 jobs created between January and April. June marked the first month of negative job growth since 2020. While this trend warrants attention, the combination of low unemployment and slower job creation suggests a shrinking labor force growth rate, with many employed individuals holding onto their positions. Nevertheless, this creates a difficult environment for those looking to change jobs or enter the workforce.

In response to these labor market dynamics, the Federal Reserve cut interest rates by 0.25% in the quarter, bringing its target range to 4.00%–4.25%. The Federal Reserve cited downside risks to employment as the primary reason for the cut. With its dual mandate to promote full employment and maintain low inflation, the Federal Reserve has shifted its focus toward supporting the job market while maintaining a close eye on the inflation picture.

Looking ahead, the Federal Reserve’s latest projections suggest two additional rate cuts may occur this year. In response, the 10-year Treasury yield—a key benchmark for borrowing costs—has declined to 4.1%. As interest rates fall, bond prices rise, and U.S. bonds have responded positively. 2025 is shaping up to be the strongest year for U.S. bonds since 2020, when rates were cut in response to the pandemic. Mortgage rates have also declined, offering relief to homebuyers and homeowners seeking to refinance.

Rate cuts have also benefited emerging markets by easing pressure on their currencies. China’s stock market, the largest in the emerging market category, rose 19.5% in the third quarter and is now up over 41% for the year. Taiwan and South Korea posted strong quarterly gains of 10.8% and 11.6%, respectively. These economies, with their innovative technology sectors, are capitalizing on global AI investment and robust export demand. With returns now over 30% for the year, 2025 is shaping up to be the best year for emerging market stocks since 2017.

As is typically the case, investors today are confronted with a mix of positive and negative economic and investment signals. This is not any different from years past. The road to investment growth is rarely wiped clean of at least some potholes and cracks. Despite this uncertainty, both stocks and bonds are up, and investors with balanced portfolios are now enjoying their third consecutive year of positive returns across all major asset classes. This performance underscores a key principle: markets reward those who stay the course through uncertainty. This perseverance does not require blind optimism but rather thoughtful preparation. To that end, we will continue to manage your portfolio to perform across a range of market conditions and position you to both capture opportunities all while managing risk.

Sincerely,

Your Harbor Group Team

2025 Second Quarter Investment Report

2025 First Quarter Investment Report